Introduction: A Few Key Differences in California Taxation

Perhaps you’ve heard about the benefits of structuring your entity as an S- corporation after reading one of our articles or elsewhere. As we mentioned in “S corporations: Advantages and Disadvantages,” one of the main advantages of structuring as an S-corporation is that it is a flow-through entity for federal income taxation purposes.

This means that the taxation “flows through,” or bypasses the entity level to the shareholders. Since the individual shareholders rather than the entity itself are taxed, S- corporations are an attractive alternative to corporations, which pay taxes both at the entity level and the individual shareholder level.

The draw of avoiding double taxation is largely why businesses structure themselves as S- corporations, and yet this is exactly where California differs from many other states’ tax treatment of S- corporations.

Setting Up an S Corp in California – What You Need to Know

In California, S- corporations are subject to an annual minimum franchise tax at the entity level on their net income. As a result, any S-corporation in California’s jurisdiction must pay whichever number is greater of $800 or 1.5% of their annual net income to the California Franchise Tax Board (FTB), unless they are newly incorporated that year.[1]

In addition, individual shareholders must pay California income tax on any gains distributed from the S- corporation. If the point of making an S- election is to eliminate any state or federal income taxation at the entity level, at first glance, the California tax regime seems to nullify the point of making an S- election to become an S- corporation. Right?

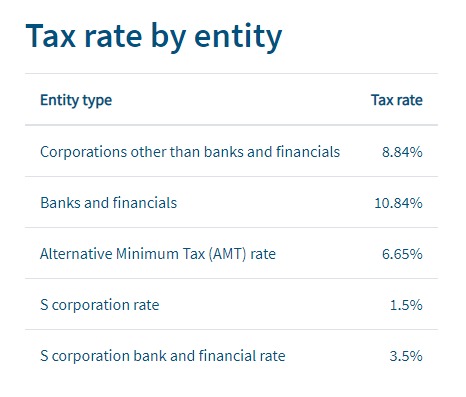

Consider this chart created by the FTB:

Source: https://www.ftb.ca.gov/file/business/tax-rates.html

Corporations are still subject to a higher tax rate at the entity level than S- corporations. Therefore, it may still be beneficial from a tax standpoint to structure a business as an S- corporation in California.

Two other differences in how California taxes S- corporations may prove beneficial: California S- corporations are allowed both tax credits and net operating losses.[2]

How to Determine Jurisdiction in California

From a tax standpoint, an S-corporation will likely pay less in taxes if it does not fall under California’s jurisdiction. While determining jurisdiction is an important consideration for determining the tax consequences of a business, it also impacts employee benefits, such as the type of retirement and health plans that the business should choose.

Several factors play a role in determining jurisdiction in California:[3]

- Location: are the company’s offices located in California?

- “Doing business:” does the company conduct its operations in California?

- Type of business: what kind of business does the S- corporation plan to operate? California regulates some kinds of businesses more stringently than others, so a state’s regulations or lack thereof should be a consideration both when starting a new business and buying a business located in California.

California Tax Law’s Impact on S- Corporations Involved in F Reorganizations

In our article, “Alphabet Soup: When S-corporations Meet F Reorganizations,” we discussed how QSubs are used to achieve a tax-free reorganization of an S- corporation. Specifically, a QSub is a disregarded entity, meaning that for tax purposes it is considered the same entity as its parent S Corporation.

Because California tax rules would still treat the QSub as a disregarded entity, some wrinkles must be considered. Since the QSub is disregarded for tax purposes, all of its business activities, assets, liabilities, income, and credits are considered as if they are part of the S Corporation.[4]

As a result, if the QSub falls under California’s jurisdiction, the parent S Corporation would be subject to the minimum franchise tax of $800 or 1.5% of annual income.

This tax applies even if the S corporation itself does not fall within California’s jurisdiction. Buyers considering purchasing an S-corporation with a Q-Sub in California should therefore be aware of this California tax liability.

California Tax Law’s Impact on S- Corporations Involved in Asset Sales & 338(h)(10) Elections

In our previous articles, including “The Unicorn of M&A: 338(h)(10) Elections” and “Asset Sales vs. Stock Sales”, we’ve discussed the tax consequences of asset sales, stock sales, and 338(h)(10) elections.

Our discussion on 338(h)(10) elections transactions, which are structured as an asset sale, focused on how the tax benefit to the buyer may often surpasses the seller’s costs.

The same is true of other asset sales. However, the opposite is true when the target S corporation shareholders reside in a state without income taxation but the target S corporation itself is subject to tax in California.[5] Consider the following scenario:

Bobby Axelrod is a shareholder in Axe Capital who is planning to move from New York Florida, a state without income taxation, because he is tired of paying income taxes.

Let’s say Axelrod is the majority shareholder in a California S-corporation that is being sold to Mike Prince, his rival. Prince wants to structure the purchase with a a 338(h)(10) election, mostly because he knows that it will annoy Axe to have to pay a hefty chunk of change in income tax on the gain realized from the sale.

An asset sale or 338(h)(10) transaction would be a deal-breaker for Axe.

What’s Axe to do? He still wants to sell his S- corporation and Mike Prince wants his stepped up basis and stick it to Axe in the process. At this point, Axe has two options.

Options:

- Find a new buyer who will agree to do a stock sale.

- Plan ahead and do an F Reorganization of the S- corporation when Axe moves to Florida.

In the process of the F Reorganization, the S- corporation would transfer its assets to a new LLC based in Florida. Since an LLC is also a flow through entity, Axe would pay far less in taxes.

If he chooses to treat the LLC as a partnership or a sole proprietorship, Axe would not pay entity level or individual income taxes to the Florida Department of Revenue.[6]

Instead of paying California state taxes on gain from the S- corporation and federal income taxes, Axe would only pay federal income taxes on the gain from the sale of the LLC to Mike Prince.

Conclusion

As the example above demonstrates, setting up a business outside of California is usually a wiser strategy for tax purposes. There are, of course, business reasons outside of taxes to establish a business or undertake a merger or acquisition in California.

Avoiding California solely for tax reasons would also mean missing out on one of the largest economic markets in the world and in the United States. Pre-pandemic, Forbes estimated that California’s economy was the fifth largest worldwide and represents 15% of the American economy.[7]

If you are planning to buy a business that has operations in California or similar connections in that state, be cognizant of the possible tax consequences and enlist the help of tax advisers to help plan the most tax-efficient way to undertake the transaction.

Other relevant articles: “S corporations: Advantages and Disadvantages,” “A Due Diligence Minefield: Navigating S- Corporation Classes of Stock,”“Alphabet Soup: When S-corporations Meet F Reorganizations”

[1]Cal. Rev. & Tax. § 23802 (c).

[2]Cal. Rev. & Tax. § 23802(d).

[3]Cal. Rev. & Tax. § 23800.5 California [Application of IRC Sec. 1361].

[4] Cal. Rev. & Tax. § 23800.5 California [Application of IRC Sec. 1361].

[5] Andy Torosyan & Justin Bowen, U.S.C. Tax Institute, Structuring the Acquisition of an S Corporation to Achieve an Asset Basis Step Up, (June 21, 2016), available at https://www.hcvt.com/media/publication/49_Structuring%20the%20Acquisition%20of%20an%20S%20Corp_Torosyan_Bowman_2016.pdf

[6]Limited Liability Companies, Florida Department of Revenue, https://floridarevenue.com/taxes/taxesfees/Pages/rt_llc.aspx

[7] Best States for Business 2019: California, Forbes,https://www.forbes.com/places/ca/?sh=75032e7a3fef